Whether you live in a rowhouse in New Dorp, a semi-detached house in Tompkinsville, a single-family home in Mariners Harbor, or a condo in Stapleton, the “Trial Period Plan” (TPP) can feel like a major victory when you receive one from your lender. However, for many Staten Island Homeowners, the trial period is actually the most hazardous part of the foreclosure process. It is not uncommon for a homeowner to lose his/her home due to what could have easily been avoided “paperwork” errors by the lender that ultimately disqualified them from the trial period. Here are some common mistakes that Staten Island homeowners make during the Loan Modification trial period, and some helpful advice on how to stay safe and successfully complete this difficult process.

1. Failing to make payments on time during the trial period

Most of the time, failing to make a timely payment during a trial period results in the trial being terminated. In fact, paying late even once during the three months of the trial period will result in termination of the trial.

Why? Because lenders’ computers and accounting software automatically terminate trials after one late payment. Once terminated, there is little recourse for the homeowner. Therefore, it is essential to set reminders to make sure timely payments are mailed by check or paid electronically.

What can you do instead?

To prevent a delayed payment from terminating your trial, make timely electronic payments. If you cannot send an electronic payment, then mail your payment using a trackable delivery service such as fedex or ups.

If you still wish to make a cash payment, go to a nearby branch of your lender and have the cashier give you a receipt showing that you made the payment. This way, you will have proof of making timely payments and can document each payment.

2. Making changes in your income or credit status

During the four months of the trial period, Banks may perform additional background checks. Lenders usually perform a “soft pull” of your credit history and/or obtain information regarding your employment status verbally.

Why is this important?

Because of the way lending regulations work in New York State, Banks are able to evaluate whether you qualify for a modified loan based upon your current income and Debt-to-income ratio. Banks can deny your application for a modification if your credit profile worsens or if you acquire too much more Debt during the three months of the trial period.

What should you avoid doing?

Avoid taking out new lines of credit; take out new loans; do not open new accounts; do not finance personal items; and do not purchase anything else on credit. If you want to finance something big—such as buying a car—you should wait until after the trial period is over.

3. The statute of limitations trap

New York law limits the amount of time a lender has to bring a foreclosure action against a borrower. Although the law is clear that lenders cannot file suit in order to start foreclosure proceedings on older mortgages (the law gives borrowers six years), recent court decisions (Temple v Bank of America) have given lenders another opportunity to begin foreclosure actions if they sign a modification agreement.

Why does this matter?

Although lenders are prohibited from filing suit on older foreclosure cases in New York, signing an agreement to modify an existing mortgage can potentially extend the statute-of-limitations deadline and allow a lender to start again on bringing a foreclosure lawsuit against the homeowner.

What should I do?

Before agreeing to sign any type of modification agreement, especially if your mortgage is several years old and nearing its statute-of-limits deadline, you should seek guidance from an experienced lawyer specializing in foreclosure defense.

4. Failure to attend Mandatory Settlement Conferences

When a lender initiates a foreclosure proceeding against you in New York State, you are required by law to appear at certain settlement conferences. Although attending settlement conferences seems unnecessary since you are participating in a trial period plan (TPP) with your lender, failure to attend these mandatory settlements can create serious problems for homeowners.

Why are these meetings so important?

These meetings are called “Mandatory Settlement Conferences.” when you fail to attend these conferences, and your lender subsequently denies your request for a permanent modification, your case may be transferred from the “settlement part” of court where your lender has less flexibility in pursuing your foreclosure than they would otherwise have in other parts of the courthouse.

What should you do?

Even though you are participating in a trial period plan with your lender, never miss your mandatory settlement conference dates. Be prepared to explain why you are currently engaged in negotiations with your lender.

5. Failure to Return the Final Notarized Contract

When you complete four months in your trial program, it appears as though you have won, however you have yet to win until you receive and sign your permanent contract documents. It is also important to note that even though you made each required payment during those four months, you did not earn a permanent modification unless you received and signed your permanent document(s).

The Mistake: Believing that once you complete making payments, your trial payments will simply continue indefinitely.

The Consequence: Once you have completed four months of trial payments, the lender will forward to you a collection of Permanent Modification Documents. Often these packages contain documents that require signatures and/or notarizations and have an expiration date. If you fail to respond timely and correctly, the lender will notify you that you refused their offer.

The Fix: When you receive your package containing your permanent documents, review it carefully. If your package contains items requiring notarization, many local pharmacies or banks offer notary services. Mail your response using overnight express delivery and keep record of tracking information.

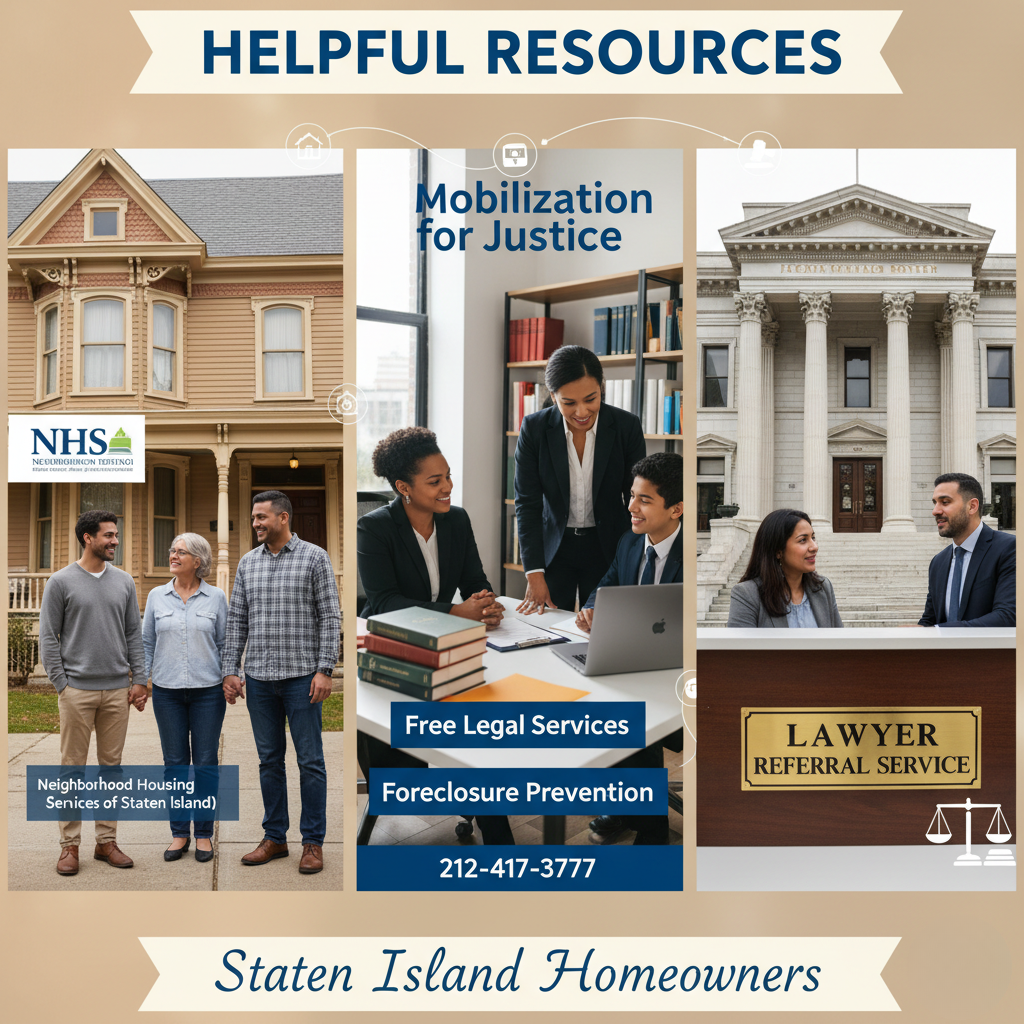

Staten Island Homeowner Resources:

Neighborhood Housing Services (NHS) of Staten Island: Located at 770 Castleton Ave. They provide free HUD-approved housing counseling and can talk to the bank on your behalf. (Phone: 718-442-8080)

Mobilization for Justice (MFJ): They provide free legal services for Staten Island homeowners facing foreclosure and can help with trial period disputes. (Phone: 212-417-3777)

Richmond County Bar Association: If you need a private attorney who specializes in foreclosure defense, they can provide a referral. Homeowners can request a referral via their website or by calling 718-442-4500

A trial period is a test of compliance, not just money. Stay diligent, keep every receipt, and don’t stop fighting until you have a signed, recorded permanent modification in your hands.

Frequently Asked Questions (FAQ)

Q: How will a missed trial payment affect me?

A: Generally, in a Trial Period Plan (TPP), there is little or no grace period. For example, if a trial payment of $400 was due on August 1 but did not arrive until August 2, it would be viewed as a “Failed Trial.” The sooner you reach out to your housing counselor or attorney, the better they will be able to assist with obtaining a “Re-Evaluation” of your case prior to the lender moving forward to resume the foreclosure process.

Q: Do I still need to appear for a Settlement Conference if I’m currently in a Trial Modification?

A: Yes. Just because you’re currently in a Trial Modification does NOT mean you get to skip your Staten Island Settlement Conference. It’s VERY important that you advise the Court Referee that you are currently participating in a TPP so that he/she can keep track of whether or not the lender is acting in good faith when attempting to convert you into a Permanent Modification.

Q: Will having a Loan Modification negatively impact my Credit Score?

A: When you enter into a loan modification agreement, most lenders will indicate the terms of the agreement as being paid “under a partial payment agreement”, and therefore may temporarily lower your credit score. Once the permanent modification has been recorded and you’ve returned to “Current Status,” your credit score should begin to improve much faster than if you had gone through a foreclosure sale.

EN

EN

RU

RU