Can You Be Foreclosed On If You Have Equity in Staten Island?

Many Staten Island homeowners believe that having significant equity in their homes acts as a protective shield against foreclosure. However, this is often a misconception. Equity is the dollar amount of your home’s value that you actually own, free from any mortgage debt. For example, if your Staten Island home is valued at $800,000 and you owe $400,000 on your mortgage, you possess $400,000 in equity. The crucial point is that lenders primarily focus on your ability to make regular mortgage payments, not the amount of equity you hold. As long as you meet the terms of your mortgage agreement, including timely monthly payments, your loan is considered current. Falling behind on these payments triggers a **default**, a serious situation that can lead to foreclosure, regardless of how much equity you have. The bank’s primary concern is recovering their investment, and timely payments are the key to that. Defaulting means they will initiate foreclosure proceedings to regain possession of the property and recoup the outstanding balance.

Common reasons homeowners with substantial equity in Staten Island properties still face foreclosure include:

- Job loss or unexpected unemployment

- Business slowdown or failure

- Increases in adjustable-rate mortgage payments

- Divorce or separation

- Unforeseen medical expenses

- Rising property taxes and homeowner’s insurance costs

This situation is often described as being “house rich and cash poor.”

While your home may represent significant wealth on paper, if you lack the liquid assets to cover your next mortgage payment, you are financially vulnerable. Equity cannot pay your bills or make up for missed mortgage installments. Lenders require tangible, readily available funds for payments; they are not concerned with your home’s paper value. Having equity does not grant you leverage with a loan servicer who operates under strict timelines and requires immediate payment.

What Happens to Your Equity During Foreclosure in New York?

Understanding the reality of foreclosure sales in New York is crucial:

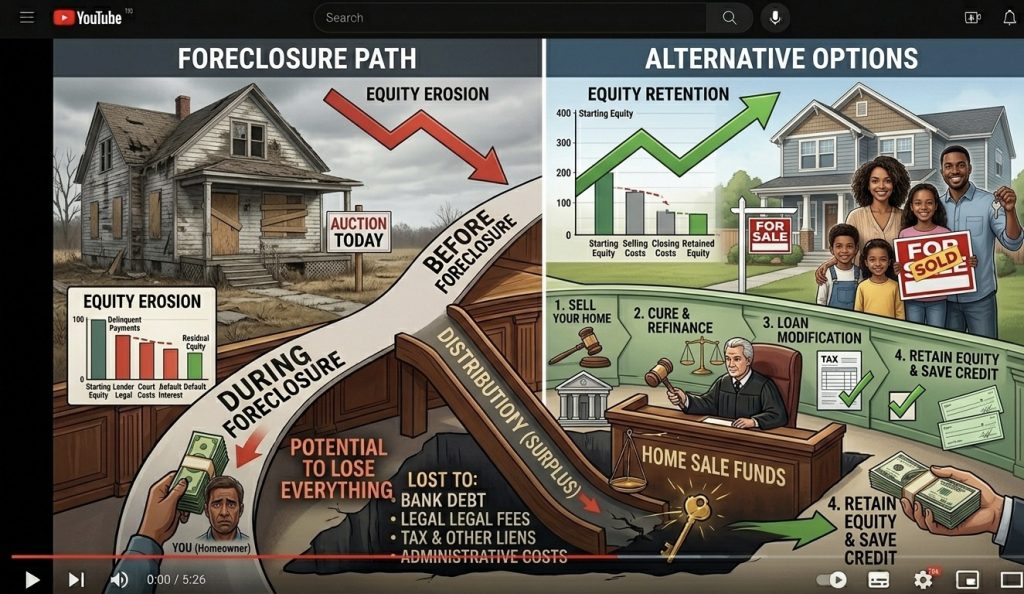

- Surplus Funds Are Rare. In a typical mortgage foreclosure auction, properties are often sold at a significant discount compared to their fair market value. Banks also add accumulated interest, late fees, legal costs, and referee fees to the outstanding debt. These combined costs frequently meet or exceed the auction price, making the realization of true “surplus funds” (where the sale price exceeds the total debt) an uncommon occurrence.

Many homeowners fear losing all their equity during foreclosure, and this fear is often justified. While legally, you’re entitled to any proceeds exceeding the total debt owed, foreclosure auctions rarely achieve market-rate prices. The urgency of the sale, steep discounts, and escalating legal fees mean that a homeowner who believed they had substantial equity might end up with very little, or nothing at all.

Can Selling Your Home Before Foreclosure Save Your Equity?

Yes, selling your home proactively can help you preserve your equity. If you foresee difficulty in meeting your mortgage obligations, listing your home on the market is a viable strategy. A traditional sale allows you to control the process, sell your property at its fair market value, and **pay off the mortgage in full**. Any remaining proceeds from the sale are yours to keep. Selling before a foreclosure sale not only protects your credit score but, more importantly, allows you to **retain the equity you’ve worked hard to build**, rather than losing it to auctioneers and legal fees.

Foreclosure Red Flags to Watch For

Foreclosure proceedings can seem slow, but they follow a legal process with clear warning signs. If you notice any of the following, it’s essential to **act quickly**:

Missed Payments: Even a single missed payment can alert your lender.

Escrow Account Changes: An unexpected increase in your mortgage payment due to escrow adjustments needs prompt attention.

Collection Calls: Receiving collection calls from your lender is an urgent sign.

Loss Mitigation Letters: These letters offer alternatives like loan modifications but have strict response deadlines.

Lis Pendens: This public notice signifies that a foreclosure lawsuit has been filed against your property, indicating time is running out.

The most significant error homeowners make is assuming their equity protects them from foreclosure. Equity is only a safeguard if you leverage it effectively before the lender forecloses.

If you’re facing financial difficulties, do not wait for your lender to initiate action. Explore options like loan modifications, refinancing, or selling your property to access your hard-earned wealth. Taking proactive steps can help you preserve your financial stability and your equity.

Foreclosure occurs when a borrower fails to meet their mortgage obligations. The primary factor is not home equity, but rather the consistent fulfillment of responsibilities, specifically making regular mortgage payments. As long as payments are current, a homeowner’s equity is generally not at risk. However, once payments are missed, the lender’s priority becomes recovering the outstanding debt through foreclosure. Here’s a simplified outline of the foreclosure process:

- Missed Payments: The initial trigger for potential foreclosure.

- Notice of Default: After several missed payments, the lender files a formal notice, creating a lien on the property.

- Public Auction: Typically several months later, the property is sold at auction to recover the owed amount.

- Vacating the Property: If the new owner does not vacate, eviction procedures may follow.

The Biggest Mistake Homeowners Make

The most critical error a homeowner can make is believing that substantial equity shields them from foreclosure. Equity is only a safety net if you understand how to utilize it before the bank initiates foreclosure proceedings.

If you’re experiencing financial hardship, don’t delay until your lender takes action. Understanding and acting on your options—whether it’s modifying your loan, refinancing, or selling your property to access your hard-earned wealth—is crucial for preserving your peace of mind and your equity. Contact Supreme Home Sales today to discuss your options for selling your Staten Island home and protecting your equity.

EN

EN

RU

RU