Is Mortgage Forbearance a Good Idea? The Hidden Moment Most Homeowners Miss (NY & NJ Homeowners’ Guide)

If you live in New York or New Jersey, it starts with a simple piece of paper, a notice that most people don’t recognize for what it really is. You open it (if you do), and the language feels distant, almost bureaucratic. Words like “pending action,” “lis pendens,” “default,” float across the page. It doesn’t sound urgent. But it is.

That’s the first hidden moment in most foreclosure stories, the moment when action could still save your home.

And it’s also the moment where many homeowners ask themselves:

“Is mortgage forbearance a good idea?”

Let’s talk about that, not in legal jargon, but in real terms, with facts grounded in the laws of New York and New Jersey, and empathy for what you’re actually living through.

Understanding the Real Beginning of Foreclosure

Most homeowners think foreclosure starts when the sheriff shows up or when the auction date is posted online. The truth?

In New York and New Jersey, it begins much earlier, with a legally required notice.

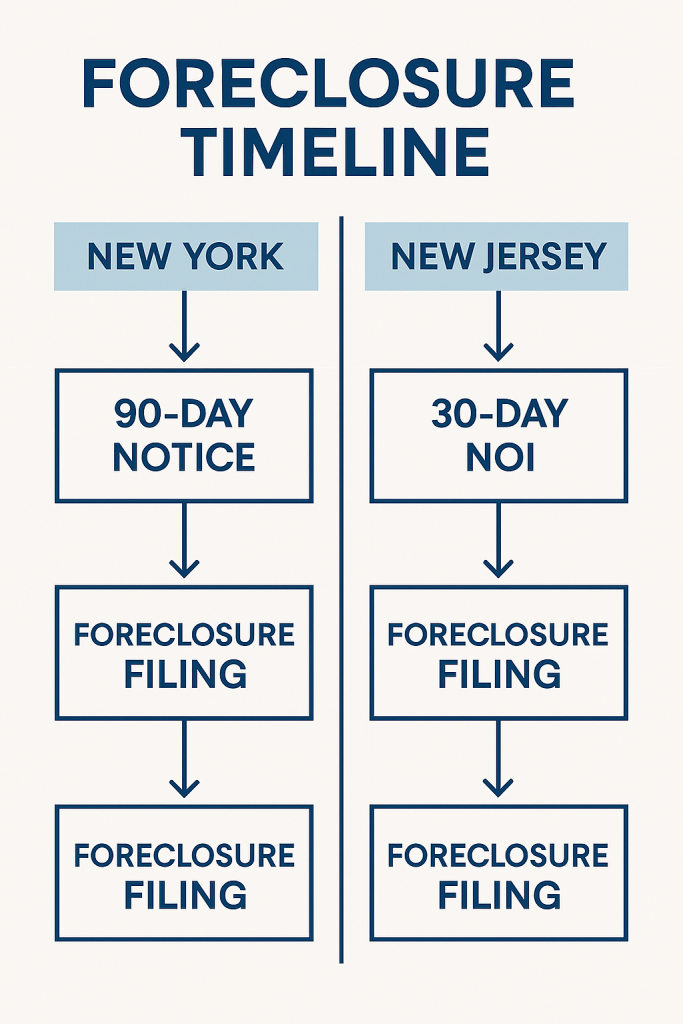

In New York: The 90-Day Pre-Foreclosure Notice

Under RPAPL §1304, before any bank or mortgage servicer can file a foreclosure lawsuit, they must mail a 90-day Pre-Foreclosure Notice to the borrower. It must be sent by both certified and first-class mail, and it must clearly state:

- That you’re in default on your mortgage.

- The exact amount needed to bring your loan current.

- That you have 90 days before the lender can file a foreclosure case in court.

- And — most importantly — it must include a list of at least five HUD-approved housing counseling agencies near you.

If you get this notice, you’re not yet in court, but the countdown has begun. (nycourts.gov)

In New Jersey: The Notice of Intention to Foreclose

In New Jersey, things move a little differently. Under the Fair Foreclosure Act (N.J.S.A. 2A:50-56), your lender must send a Notice of Intention to Foreclose (NOI) at least 30 days — but no more than 180 days — before they can file the lawsuit.

The notice must:

- State why the lender plans to foreclose.

- Show the total amount you owe to reinstate the loan.

- Identify who currently owns the mortgage.

- Inform you of your right to cure the default (catch up).

Once that 30-day period passes, the lender can file the foreclosure complaint in court. From there, the process becomes judicial — formal, legal, and often expensive.

So if you’re holding one of these notices right now, you’re not “safe until the sheriff shows up.”

You’re already standing at the starting line. And if one of the options you were dealt with is Forbearance, keep reeding.

So, Is Mortgage Forbearance a Good Idea?

That’s the million-dollar question — and the answer depends on where you stand in the process.

When Forbearance Can Help

Forbearance can be a lifeline when:

- You’re facing a temporary hardship (job loss, medical issue, family emergency).

- You expect your income to recover within a few months.

- You’re not yet deep into the court process.

- You use the forbearance period to strategize, not hide.

In essence, forbearance means your lender lets you pause or reduce payments for a set time — typically three to six months. During this pause, you’re not off the hook for what’s owed, but you gain breathing room.

You can use that space to:

- Seek a loan modification or refinance.

- Consult a housing counselor.

- Explore pre-foreclosure sale options to protect equity

When Forbearance Becomes a Trap

Forbearance can backfire if:

- You’re already in foreclosure litigation and assume the pause will “freeze” it (it won’t).

- You misunderstand how repayment works — those skipped payments come due later.

- You let the pause lull you into further inaction.

- You fail to confirm the terms in writing.

It’s not that forbearance is bad — it’s that many homeowners treat it like a cure, when it’s really a bandage.

In both New York and New Jersey, your lender must still follow court timelines. That means if a complaint has been filed, the court case continues unless a settlement or modification halts it.

So the right question isn’t just “Is mortgage forbearance a good idea?”

It’s: “Is it the right idea for me — right now?”

What to Do the Moment You Realize You’re in Trouble

Here’s what I tell every homeowner who finds that plain, unfamiliar envelope on their counter:

1. Open the Letter

Whether it says Pre-Foreclosure Notice (New York) or Notice of Intention to Foreclose (New Jersey), you must read it. Identify the date and note how long you have — 90 days in NY, 30–180 days in NJ.

2. Call a HUD-Approved Housing Counselor

These professionals are trained to help homeowners for free or at low cost. They can:

- Explain what the notice means.

- Contact your servicer with you.

- Help prepare modification or forbearance requests.

Find one through the HUD website or by calling (888) 995-HOPE.

3. Contact Your Lender or Servicer Directly

Ask these questions:

- “If I enter forbearance, will interest continue to accrue?”

- “How will missed payments be handled afterward?”

- “Will you report this to credit bureaus?”

- “Can I combine forbearance with a modification later?”

Always get answers in writing.

4. Respond to the Court if You’re Already Sued

If you live in New York, you’ll likely receive a Summons and Complaint after the 90-day period. You must file an Answer with the court — attending a settlement conference doesn’t replace that.

In New Jersey, once the complaint is filed, you must also file an Answer within 35 days. Missing it means the bank can proceed without your side being heard. (NJ Courts Self-Help Center)

5. Act Before Judgment

If keeping the home isn’t realistic, consider selling before the judgment is entered.

A pre-foreclosure sale often preserves more equity than waiting until an auction, when legal costs have ballooned.

The Legal Framework You Need to Know

| Step | New York | New Jersey |

|---|---|---|

| 1. Pre-Foreclosure Notice | 90-Day Notice under RPAPL §1304; sent certified + first-class mail. | Notice of Intention to Foreclose (NOI) under N.J.S.A. 2A:50-56; at least 30 days before suit. |

| 2. Court Filing | Complaint + Notice of Pendency (lis pendens) filed in Supreme Court. | Complaint filed in Superior Court; case becomes lis pendens. |

| 3. Homeowner’s Response | Must file Answer (within 20 days if served personally, 30 days if by mail). | Must file Answer within 35 days of service. |

| 4. Settlement/Mediation | Mandatory Settlement Conference under CPLR §3408. | Voluntary mediation through NJ Courts Self-Help Program. |

| 5. Judgment & Sale | Foreclosure Judgment → Sale within 90 days (RPAPL §1351). | Final Judgment → Sheriff’s Sale (timing varies by county). |

Five Lessons from Homeowners Who Waited Too Long

- The notices are real, even if they don’t look urgent.

In both NY and NJ, the legal process starts with ordinary-looking mail. - Forbearance buys time, not immunity.

If you’re already in litigation, the lawsuit keeps moving unless you act. - Equity is the first casualty of delay.

Every legal fee and late charge comes from your equity. - Early action creates leverage.

The sooner you respond, the more negotiating power you keep. - Hope is not a plan.

You need a written plan — whether that’s modification, sale, or repayment.

It’s Not Over Yet

If you’re reading this, chances are you’re tired — of letters, of uncertainty, of fear.

But here’s the truth: you still have time.

Whether you choose to fight for your home, negotiate a modification, or sell on your own terms, the power comes from understanding the process.

Is mortgage forbearance a good idea?

Yes — if you use it as a bridge, not a blindfold.

Yes — if it helps you plan your next move, not postpone it.

Yes — if you combine it with action.

The worst decision you can make is silence. Because once the court keeps moving without you, what could have been saved is often lost.

So open the letter. Call the counselor. Talk to your lender.

You still have time — but only if you use it.

FAQ — Quick Answers for NY & NJ Homeowners

Q1: How do I know if I’m officially in foreclosure?

If you’ve received a Summons and Complaint, the case is filed. In NY, it follows the 90-day notice. In NJ, it follows the NOI.

Q2: Can I stop a foreclosure once it’s filed?

Yes — through a loan modification, forbearance agreement, or sale before judgment. The earlier you act, the more options remain.

Q3: Does forbearance hurt my credit?

Usually not if it’s a formal agreement and payments resume as agreed, but always confirm how your servicer reports it.

Q4: What’s the difference between forbearance and modification?

Forbearance pauses payments temporarily; modification permanently changes your loan terms (interest rate, term length, or amount owed).

Q5: If I sell before the sale date, do I still owe anything?

If the sale proceeds cover your balance and costs, you’re free and clear. If not, a deficiency judgment may apply, depending on state law.

Q6: Where can I get help that’s actually free?

Visit the HUD Housing Counselor Locator or CFPB’s homeowner relief page, or call (888) 995-HOPE — a national nonprofit network offering confidential assistance.

👉 If you’re already behind on your mortgage, you can’t afford to guess. Watch this before you decide if mortgage forbearance is really a good idea, or something you’ll regret.

#mortgageforbearance #foreclosurehelp #foreclosure

Foreclosure Freedom is powered by Supreme Home Sales, Inc.

Resources for Homeowners in NY & NJ

📄 Free Hardship Letter Template → https://supremehomesales.com/sample-hardship-letter/

📘 Homeowner’s Equity Protection Guide →https://supremehomesales.com/the-foreclosure-survival-guide/

📅 Pick A Time In My Calendar and Book a Free Call Before Foreclosure Hits Hard → https://calendly.com/foreclosurefreedomdesk/30min

Receive a fair CASH OFFER without any commitment to accept. Visit: https://www.StatenIslandForeclosures.info

📱 Follow Us on Social Media:

✅ Facebook: facebook.com/EsphirPopilevsky ✅ Instagram: instagram.com/esphir_supreme_home_sales/?hl=en

✅ TikTok: tiktok.com/@realtor.esphir.nyandnj?lang=en

🤝 Join Our Community: youtube.com/c/EsphirPopilevsky

#foreclosurefreedom #stopNYforeclosure #stopNJforeclosure

Esphir Popilevsky NY & NJ Licensed Real Estate Broker NY: Supreme Home Sales, Inc. and NJ: DreamLife Realty 44 Robin Ct. Staten island, NY 10309 O: 718.689.4737 / Direct: 917.579.4455 supremehomesales@gmail.com https://www.supremehomesales.com Subscribe to this channel https://www.youtube.com/c/EsphirPopilevsky

EN

EN

RU

RU