Maybe you’re a homeowner who has fallen behind on your mortgage payments. It’s normal to want to find a quick solution. One common approach is to refinance. Lower monthly payments. Reset the loan. Fix the issue.

Sounds good. Sounds logical.

However, there are some issues with using refinancing as an answer to your financial problems, especially when time is of the essence. Here’s what most homeowners don’t know. When you try to use refinancing as a Way out of your financial problems, it rarely ends well. And, in fact, it can even waste the little bit of time you have left.

🔴 I’ve explained all of this in detail in the video below, which includes what really works and why nearly everyone gets this wrong.

📹 before reading this article watch the video first (it will make a lot more sense)

Why refinancing seems like an obvious answer (but usually isn’t)

Think about this for a moment…

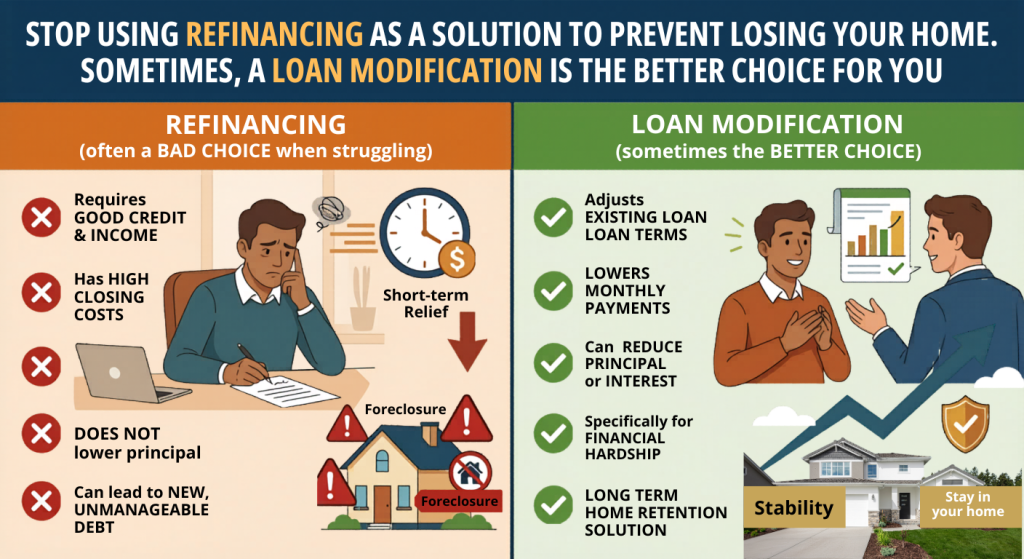

Refinancing is a whole new loan. Therefore, the bank is viewing you in relation to your current circumstances — not your past. So you are essentially asking the same bank that currently has a lien on your home for approval of a whole new loan… While you’re still having trouble making payments on your old one.

At this point, the entire process begins to unravel.

Most homeowners aren’t aware that they won’t learn this until after they have invested weeks into submitting applications, providing documentation and waiting to receive a denial.

The larger issue: Time

Here is where this process can cause serious harm.

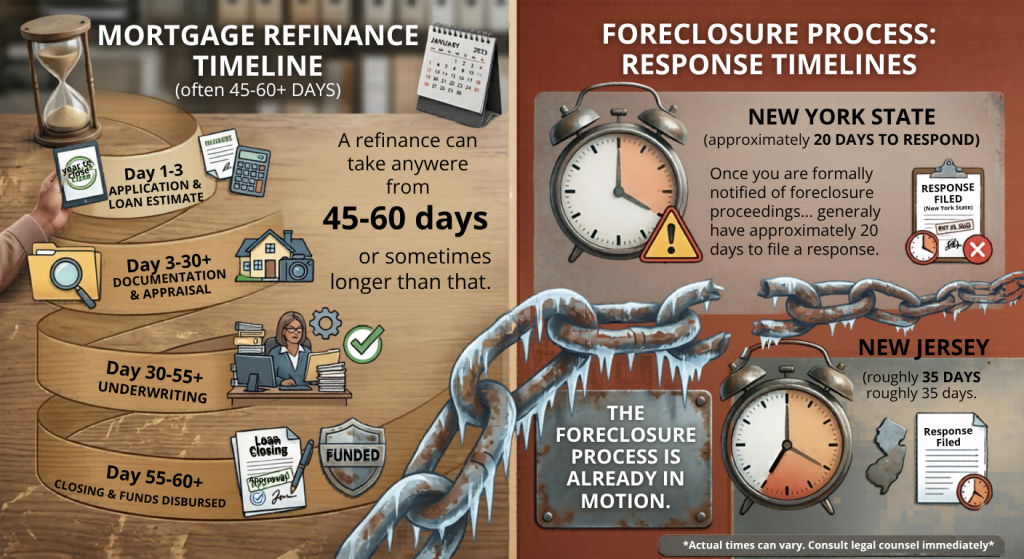

Time seems like it isn’t pressing — until it is. A refinance can take anywhere from 45-60 days or sometimes longer than that. However, the Foreclosure process is already in motion. In New York state, for example, once you are formally notified of Foreclosure proceedings you generally have approximately 20 days to file a response. In New Jersey, it is roughly 35 days.

Neither of those deadlines stop simply because you are attempting to refinance.

What ends up happening? You spend precious time trying to resolve the situation… Only to realize too late that it isn’t going to work. By then you’ll be further along toward losing control of the situation.

So what else can work instead of a refinance?

Most homeowners fail to recognize this opportunity.

Loan modification.

This isn’t a new loan. This is an adjustment to your current loan so that your payments become manageable.

With a loan modification, instead of starting fresh; you’re working within what you already have:

• same lender

• same loan

• new terms tailored to your present circumstance

Some examples include:

• extending the loan term

• adjusting the interest rate

• adding missed payments to the principal balance

The objective is straightforward.

🌟 reduce your monthly payment so you can afford it.

Why loan modifications give you something even more important than money, Time.

Once you’ve submitted a comprehensive loan modification application package, lenders are obligated to review them. That process takes time. Not always long enough to prevent foreclosures from occurring… However often enough to provide you with time to decide what action needs to be taken next.

That additional time? Most homeowners think they have it… Until they discover they don’t.

How quickly Things can go horribly wrong (even if you think you have the “right” plan)

Just like with anything else in life… Even loan modifications can go horribly wrong if they’re mishandled. I’ve personally seen scenarios where homeowners believed they were receiving assistance… Only to have Things turn completely sour.

If you’d like to see exactly how fast this can occur, I documented a true scenario that happened in Staten Island in my last video — because there’s no other Way this will work unless you follow these steps correctly.

The unseen dangers of home loan refinancing — even when you are pre-approved for it

Okay, let’s just assume you are pre-approved for a home loan refinance.

You will have likely saved money by reducing the amount of monthly payments you owe toward the value of your house.

However, there is a lot more to consider than just getting your monthly payments reduced. In fact, when you refinance your home, you typically pay Closing fees and can end up taking out a bigger loan. Therefore, even if you get pre-approved for a home loan refinance, the true issue may be how big of an impact your monthly payments will have on your ability to afford them.

Therefore, the key question is:

👉 how does that monthly payment feel?

What usually occurs as a result of getting a home loan refinance is:

It works… For a little while. Then things start changing again. And in short order, a couple of months after completing the home loan refinance, you find yourself falling behind once again — with far fewer options available to correct the problem.

Before you take any more action…

If you’re considering whether or not a loan modification would be the way to go instead of a home loan refinance, then you need to understand one important thing:

The hardship letter. This is the document upon which most individuals who apply for a loan modification are denied based on — not based on their qualifications for the modification; however, due to how they explained why they needed it.

I show you exactly how to write a hardship letter in this video so you can avoid making this same mistake.

When it comes to being behind on your mortgage, it doesn’t matter which option everyone else likes best. What matters is which option makes sense for your current situation. Unfortunately, refinancing your mortgage is often not the answer.

📹 before you do anything else; Watch my next video.

EN

EN

RU

RU