It Doesn’t Arrive With A Bang

There’s no sheriff at the door, no red stamp that says “FORECLOSURE.” But here’s what no one tells you: that plain envelope might already mark the beginning of a legal process that could take your home.

I’ve met homeowners who didn’t realize their foreclosure case had begun until months later — not because they didn’t care, but because they didn’t recognize the foreclosure notice when it came.

If that sounds like you, here’s the truth: you haven’t lost your home yet. But time is moving, whether you act or not.

What a Foreclosure Notice Really Is (and Why You Might Miss It)

What a Foreclosure Notice Actually Is (and Why It’s So Misleading)

In legal terms, a “foreclosure notice” isn’t one single document — it’s a stage in a sequence that the law requires before your home can be auctioned. But it’s that first notice that matters most.

Banks know it looks unassuming. That’s the point. The less alarming it looks, the more likely you are to set it aside.

Here’s what it really means in both states 👇

Let’s break that down.

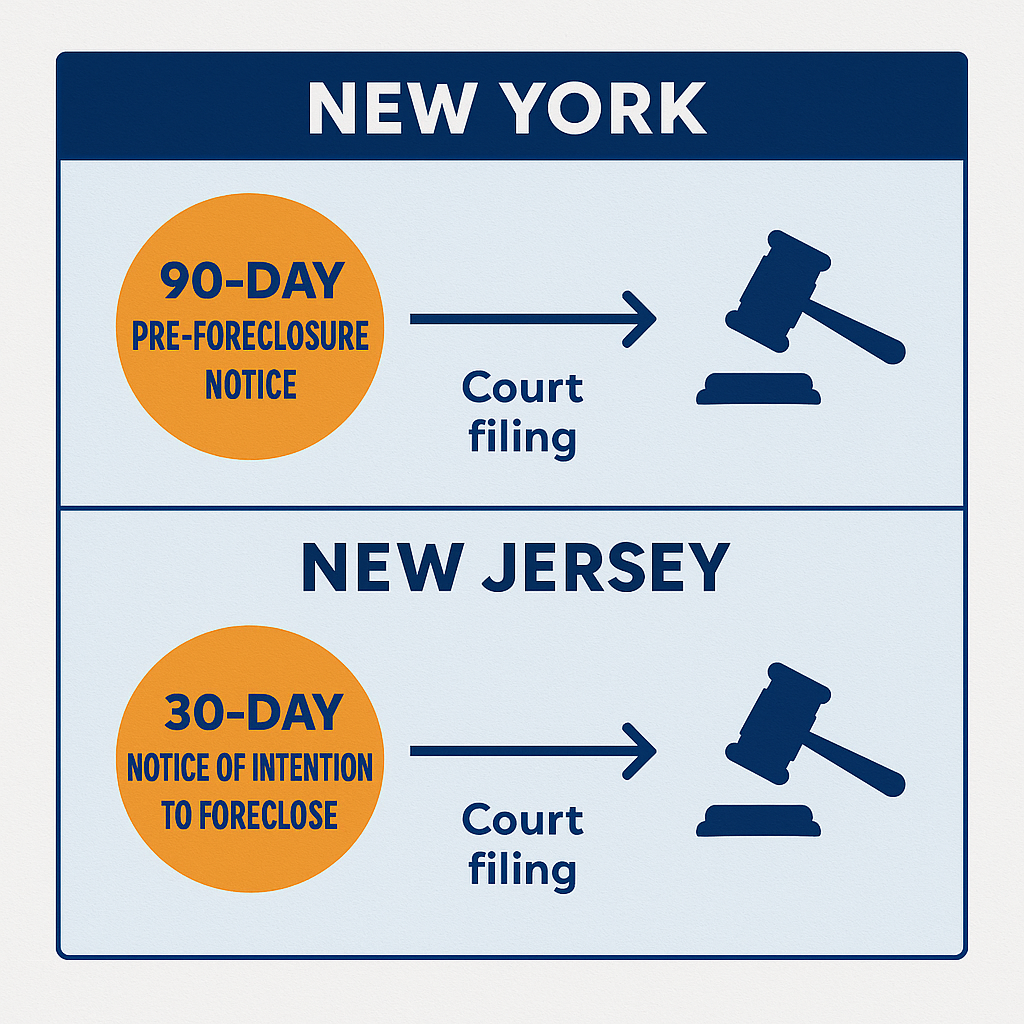

In New York: The 90-Day Pre-Foreclosure Letter (RPAPL §1304)

If your property is a 1–4 family home and your primary residence, New York law requires your lender to send a 90-day notice before they can file a foreclosure case.

That letter must:

- Tell you exactly how far behind you are.

- Inform you of the total amount due to bring your loan current.

- Provide a list of five local, HUD-approved housing counselors who can help for free.

- Be mailed by both certified and first-class mail.

If you receive this notice, the clock is ticking — but you still have a full 90 days to take action.

After that, your lender can file a foreclosure complaint in New York Supreme Court, and once that happens, your case becomes public record.

If your bank didn’t send this notice correctly, the law may actually be on your side — but you’ll never know unless you read it.

Tip: New York’s 90-Day Pre-Foreclosure Notice isn’t just a courtesy — it’s a legal requirement. If it’s missing or incorrect, your attorney can challenge the entire case.

In New Jersey: The 30-Day Notice of Intention to Foreclose

New Jersey follows the Fair Foreclosure Act (N.J.S.A. 2A:50-56), which requires your lender to give you at least 30 days’ written warning before they file a foreclosure complaint.

The Notice of Intention to Foreclose (NOI) must:

- Explain why your mortgage is in default.

- List the full amount you owe and how to cure it.

- Identify who owns your loan and how to contact them.

- Warn that the lender can file a foreclosure complaint if you don’t act.

After that 30-day window, the bank can take you to court. Once the complaint is filed, you’ll be served with a Summons and Complaint, and the case officially begins.

At that point, you still have rights — but fewer options.

Timeline check: The NOI gives you a short window to fix the problem before things move to court. Waiting even a few weeks can mean the difference between saving your home and fighting to delay an auction.

Common Mistakes That Cost Homeowners Their Homes

❌ Waiting for a phone call from the bank.

They won’t call. The law doesn’t require them to.

❌ Ignoring certified mail.

That’s where most foreclosure notices arrive.

❌ Assuming forbearance stops the case.

It only pauses payments — unless formally approved and documented.

❌ Thinking it’s too late to sell.

Until the court enters judgment of foreclosure and sale, you can still sell and protect your equity.

How Homeowners Lose Equity Without Realizing It

Here’s what most people don’t understand: foreclosure doesn’t just threaten your home — it steals your equity.

Every day that passes, interest and penalties stack up. Every filing fee, inspection charge, and legal bill gets added to your balance.

Let’s say you’ve built $200,000 in equity over the years. That’s your cushion — the money you could walk away with if you sold today.

But if you let months pass without action, the costs quietly chip away at that safety net until there’s almost nothing left.

I’ve seen it too many times.

Not because people didn’t care — but because they believed the real foreclosure notice would look different.

How to Tell You’re Already in Foreclosure (Even If No One Told You)

In both states, there are signs your case has already started — even if you haven’t received a call or court date yet.

| Sign | What It Means | What To Do |

|---|---|---|

| You received a Summons and Complaint | Your case has been filed in court. | File an Answer immediately (NY: 20–30 days, NJ: 35 days). |

| You see your name or address on the county’s online docket | A foreclosure action has begun. | Contact a housing counselor or attorney today. |

| You received a Lis Pendens or Notice of Pendency | The court has linked your property to an active case. | Respond fast to preserve your rights. |

| You’ve started receiving letters from law firms instead of your lender | The loan has been referred to a foreclosure attorney. | Communicate in writing and keep records. |

Ignoring these signals doesn’t pause the process — it only gives the bank a head start.

What You Should Do the Moment You Find the Notice

- Open It Immediately.

Don’t delay another day. Even one week of waiting can shrink your options. - Verify the Type of Notice.

- 90 days = New York Pre-Foreclosure Letter.

- 30 days = New Jersey NOI.

This tells you how much time you have before a court filing.

- Call a HUD-Approved Counselor.

These professionals offer free help and can even communicate with your lender on your behalf. - Contact Your Lender’s Loss Mitigation Department.

Ask about:- Loan reinstatement (paying what’s overdue),

- Forbearance (temporary pause or reduction),

- Loan modification (long-term change to your loan).

- If You’re Served Court Papers, Respond.

Filing an Answer prevents a default judgment and keeps you eligible for settlement conferences.- New York: Settlement conference required (CPLR §3408).

- New Jersey: Foreclosure Mediation Program available.

- Don’t Panic — Plan.

Even if you can’t keep the home, acting early lets you sell before judgment and protect what’s yours.

Why Homeowners Wait Too Long

If you’ve been avoiding the mail, you’re not lazy or irresponsible — you’re overwhelmed.

Financial hardship creates shame, and shame makes us freeze.

The banking system exploits that silence. They send the one letter that really matters looking just like all the others.

But now you know better. You’re not powerless. You’re informed — and that makes you dangerous to a system that relies on confusion.

The Bottom Line: Silence Costs You More Than Action

That envelope on your counter isn’t just paper. It’s a legal warning — and your last early chance to steer the outcome.

You don’t need to panic. You don’t need to face it alone. But you do need to act.

Every homeowner I’ve helped who opened that letter early kept something valuable — their home, their equity, or their peace of mind.

You still have time. But not if you keep waiting for the letter that says “foreclosure.”

This is that letter.

Frequently Asked Questions

Q1: Does receiving a foreclosure notice mean I’ve lost my home?

No — it means the process is starting. If you act quickly, you can still stop it.

Q2: How long do I have to respond?

- NY: 90 days after the pre-foreclosure notice, then 20–30 days after court papers.

- NJ: 30 days after the NOI, then 35 days after the complaint.

Q3: Can I stop foreclosure once it starts?

Yes — through modification, reinstatement, or sale before judgment.

Q4: How can I tell if a notice is real or a scam?

Call your lender directly and verify the address and reference number. Never wire money to third parties without confirmation.

Q5: Will ignoring the notice buy me time?

No. The case moves forward even if you do nothing. Silence benefits only the lender.

Watch this video before you open your next letter from the bank. That envelope might not be “just another notice.” It could be the foreclosure notice that changes everything.

Foreclosure Freedom is powered by Supreme Home Sales, Inc.

Resources for Homeowners in NY & NJ

📄 Free Hardship Letter Template → https://supremehomesales.com/sample-hardship-letter/

📘 Homeowner’s Equity Protection Guide →https://supremehomesales.com/the-foreclosure-survival-guide/

📅 Pick A Time In My Calendar and Book a Free Call Before Foreclosure Hits Hard → https://calendly.com/foreclosurefreedomdesk/30min

Unlock the EQUITY in Your HOME with a No-Obligation CASH OFFER! Find out if you have equity in your home at no cost. Receive a fair CASH OFFER without any commitment to accept. Visit: https://www.StatenIslandForeclosures.info

📱 Follow Us on Social Media:

✅ Facebook: facebook.com/EsphirPopilevsky

✅ Instagram: instagram.com/esphir_supreme_home_sales/?hl=en

✅ TikTok: tiktok.com/@realtor.esphir.nyandnj?lang=en

🤝 Join Our Community: youtube.com/c/EsphirPopilevsky

#foreclosurefreedom #stopNYforeclosure #stopNJforeclosure

Esphir Popilevsky NY & NJ Licensed Real Estate Broker NY: Supreme Home Sales, Inc. and NJ: DreamLife Realty 44 Robin Ct. Staten island, NY 10309 O: 718.689.4737 / Direct: 917.579.4455 supremehomesales@gmail.com https://www.supremehomesales.com Subscribe to this channel https://www.youtube.com/c/EsphirPopilevsky

EN

EN

RU

RU